In our previous article, we introduced the key principles behind the tax treatment of foreign-sourced gains from the sale or disposal of foreign assets.

To recap, foreign-sourced gains from the disposal of foreign assets (excluding intellectual property rights) are not subject to tax in Singapore—provided that the entity has adequate economic substance during the relevant basis period. This requirement is assessed at the entity level, not the group level.

This edition focuses on the economic substance requirements for different types of entities, as well as guidance on applying for an Income Tax Advance Ruling from IRAS.

Economic Substance Requirements by Entity Type

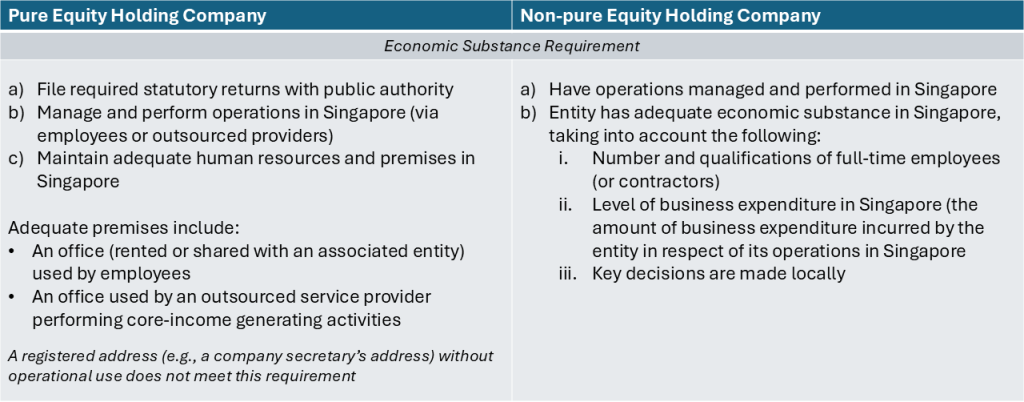

Pure Equity Holding Company

As defined in Paragraph 8.2 of the e-Tax Guide, a Pure Equity Holding Company is one that:

- Solely holds shares or equity interests in other entities; and

- Earns only

- dividends or similar payments from the shares or equity interests;

- gains from the sale of the shares or equity interests; or

- incidental income from its holding activities

Non-pure Equity Holding Company

Defined in Paragraph 8.9, these are entities that carry out activities beyond just holding investments. Their substance is assessed based on core income-generating activities in Singapore.

Outsourcing of economic activities

The economic substance requirement takes into account outsourcing arrangements where an entity outsources some or all of its economic activities to third parties or group entities.

For an outsourcing arrangement to satisfy the economic substance requirement, the following conditions must be satisfied:

- Activities must be performed in Singapore

- The outsourcing entity must exercise direct and effective control

- The outsourced service provider must dedicate sufficient resources (e.g., manhours)

IRAS will assess the Singapore-based resources of the outsourced provider, and services must be charged at arm’s-length under transfer pricing rules.

Application to IRAS for Income Tax Advance Ruling on Adequacy of Economic Substance

The foreign-sourced disposal gains from the sale or disposal of a foreign asset (other than an intellectual property right) will not be treated as income chargeable to tax in Singapore if the entity making the sale or disposal has adequate economic substance in Singapore.

To obtain certainty, Companies may consider to apply to the IRAS for an advance ruling to seek assurance on the adequacy of economic substance (known as an “ESR AR application”) if their proposed sale or disposal of a foreign asset is expected to occur within one year from the date of the application.

Application Procedure:

You may make an application on an entity basis or submit a group application. In the case of a group application, the application must be made jointly by all entities of the group to be covered under the advance ruling.

A group application may be submitted only under the following circumstances:

- where the economic activities of the entities of the group to be covered by the advance ruling are outsourced to an outsourced entity under a single service agreement; or

- where the economic substance test is to be applied at the holding company level on behalf of its special purpose vehicles.

The advance ruling on the adequacy of economic substance, if issued, may be valid for up to five (5) Years of Assessment, including the Year of Assessment relating to the basis period in which the proposed sale or disposal of the foreign assets is envisaged to take place. This means that the ruling may be applicable to the foreign-sourced disposal gains from any subsequent sale or disposal of foreign assets within the advance ruling validity period. This is provided that the relevant facts and representations made for the purpose of the ruling application remain unchanged and there is no change in the tax laws or the interpretation of the tax laws from the date of the advance ruling.

Required Documents for ESR Application

Submit the following additional documents for applications on adequacy of economic substance:

- Form for income tax advance ruling on the adequacy of economic substance (ESR Form)

- Annex to ESR form, if applicable

- A copy of the outsourcing service agreement, if applicable

- Any additional information that may assist to expedite the review of your ruling application

? For questions or help with preparing your ESR application, feel free to reach out to our team.

If you have any questions, please email to:-

Funds-related inquiries

Jocelyn <jocelyn@prestigefiduciary.com>

Zoey <zoey@prestigefiduciary.com>

Shi Ning <shining@prestigefiduciary.com>

Sales inquiries

Dong Neng <dongneng@prestigefiduciary.com>

Xiao Yan <xiaoyan@vodich.com.sg>

Clarissa <sales@vodich.com.sg>

Tax inquiries

Siew Chui <susan@vodich.com.sg>

General inquiries

Puay Siang <puaysiang@vodich.com.sg>