- Home

- /

- Accounting Tips

- /

- Understanding IFRS 18: A...

The International Accounting Standards Board (IASB) has introduced IFRS 18 Presentation and Disclosure in Financial Statements, effective from April 9, 2024. This new standard supersedes IFRS 1 Presentation of Financial Statements, addressing investors’ growing demands for enhanced transparency and detailed financial performance reporting.

What are the key changes?

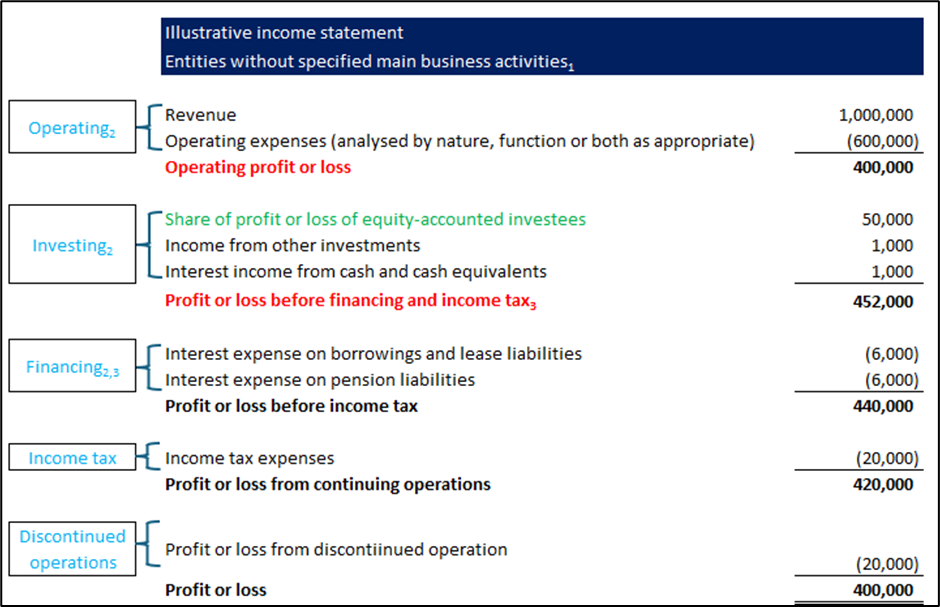

1. More structured income statement

IFRS 18 introduces some key changes for the income statement, including:

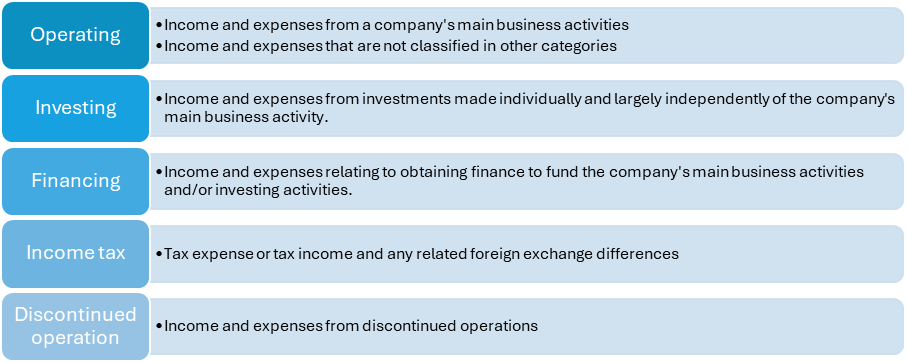

Income and expenses classified into 5 categories, depending on a company’s main business activities

Present a newly defined ‘operating profit or loss’, ‘profit or loss before financing and income taxes’ and other additional subtotals that are deemed necessary on the face of the income statement.

Required totals and subtotals

| Required totals and subtotals | Is this new? |

| Operating profit or loss Profit or loss before financing and income taxes | Yes, newly introduced by IFRS 18 |

| Profit or loss Total other comprehensive income Total comprehensive income | No, carried forward from IFRS 1. |

Other additional subtotals

Companies are required to present additional subtotals in the income statement if they are necessary to provide a useful structured summary.

- Net interest income

- Net rental income

- Net fee and commission income

- Operating profit or loss before depreciation, amortisation and impairments

- Operating profit or loss, and income and expenses from all investments accounted under equity method

- Profit or loss before income tax

- Profit or loss from continuing operations

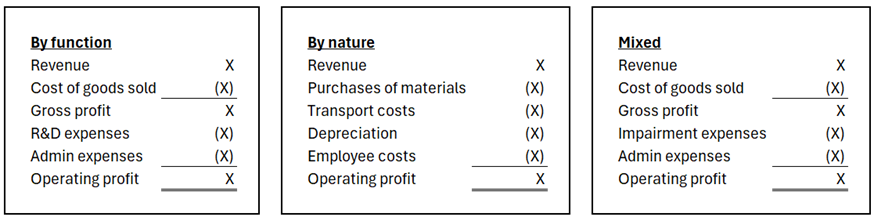

Present operating expenses either by function, by nature or on a mixed basis on the face of the income statement.

Companies might consider the following factors to determine which method provides the most useful information when analysing operating expenses either by nature, by function, or on a mixed basis.

- Main components or drivers of the company’s profitability

- The way the business is managed and how management reports internally

- Industry practices

- Allocation of expenses to functions

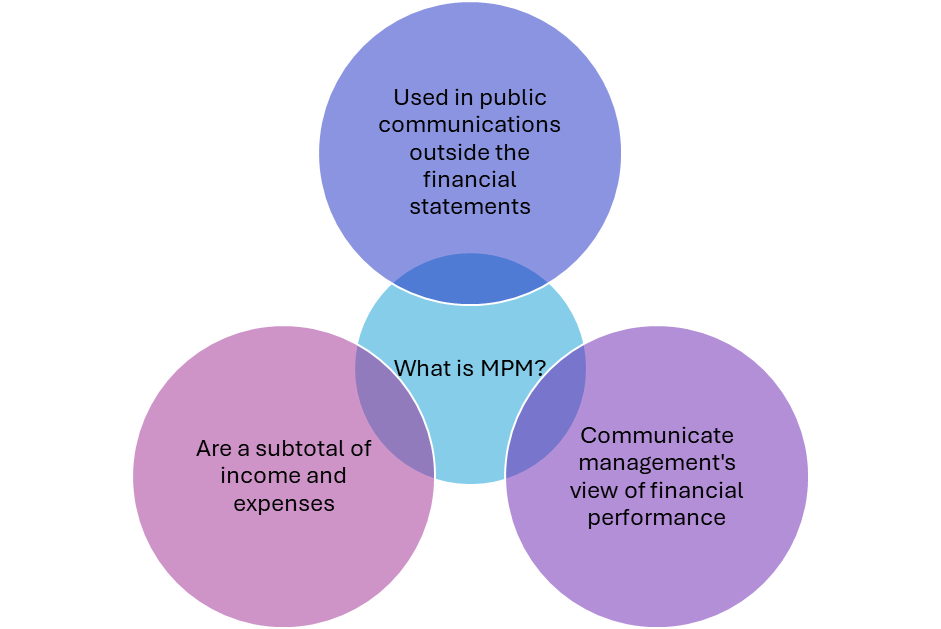

2. Management performance measures (“MPM”)

Companies are required to disclose in a single note in financial statements, that:-

- States MPM provides management’s view of the company’s financial performance and is not necessarily comparable to MPMs of other companies;

- Explains why MPM provides useful information and how it is calculated;

- Reconciles the MPM to a total / subtotal required in IFRS 18 and other accounting standards, including the tax and non-controlling interest effects for each reconciling item; and

- Explains any changes

3. Aggregation and disaggregation

- IFRS 18 introduces a new and defined role for primary financial statements.

- This role is to provide a useful structured summary of a company’s financial information that provides an understandable overview.

- Materiality continues to determine whether a company is required to present or disclose information in the financial statements.

- A company

- Aggregates assets, liabilities, equity, income, expenses or cash flows into items based on shared characteristics;

- Disaggregates items based on characteristics that are not shared;

- Aggregates or disaggregates items to present line items in the primary financial statements that provide useful structured summaries or disclose material information in the notes; and

- Ensures that aggregation and disaggregation do not obscure material information.

4. Cash flow statement

- Operating profit or loss will be the starting point when presenting operating cash flows under indirect method.

- Interest and dividend

- For companies that do not provide financing to customers or invest in assets as main business activity,

- The interest and dividend received are classified under investing activities under the amended IFRS.The interest and dividend paid are classified under financing activities under the amended IFRS.

- For companies that provide financing to customers or invest in assets as main business activity,

- The interest paid and received, and dividend received are classified under the same category as classified in income statements.

- The dividend paid is classified under financing activity.

- For companies that do not provide financing to customers or invest in assets as main business activity,

5. Balance Sheet

- IFRS 18 introduces a new requirement for goodwill to be presented as a line item in the balance sheet.

What should companies do now?

IFRS 18 is effective from 1 January 2027 and applies retrospectively. Early adoption is permitted. Now is the time to get ready.

- Assess the impacts on your financial statements

- Communicate the impacts with investors

- Consider how the new requirements impact financial reporting systems and processes.

- Monitor any changes in the local reporting landscape.